Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

Basic Question 9 of 11

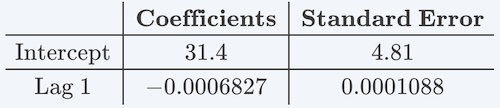

Consider the following output of an AR(1) model.

The mean-reverting level is closest to:

User Contributed Comments 0

You need to log in first to add your comment.

Your review questions and global ranking system were so helpful.

Lina

Learning Outcome Statements

describe the structure of an autoregressive (AR) model of order p and calculate one- and two-period-ahead forecasts given the estimated coefficients;

explain how autocorrelations of the residuals can be used to test whether the autoregressive model fits the time series;

explain mean reversion and calculate a mean-reverting level;

contrast in-sample and out-of-sample forecasts and compare the forecasting accuracy of different time-series models based on the root mean squared error criterion;

CFA® 2025 Level II Curriculum, Volume 1, Module 5.