Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

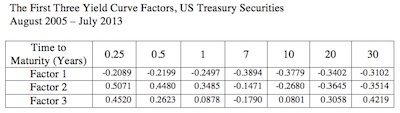

Basic Question 10 of 12

Which factor is most likely the change in the yield curve level?

A. Factor 1

B. Factor 2

C. Factor 3

User Contributed Comments 2

| User | Comment |

|---|---|

| ashish100 | Wtf wish they'd explain this better. AN please explain 100 dollars don't grow on trees brah |

| davidt87 | ashish100 i'm hating this section too. i guessed it because i assume a change in level of the curve will impact each rate in the same direction, and all of Factor 1 values were negative. Factor 2 appears to be steepness as you can see the shorter term rates are positive while the longer terms are negative - if you imagine how that would change a graph I think it would flatten it Factor 3 appears to be curvature because the middle is sinking and the short/long term values are positive Disclaimer: i have no fcking clue whats going on in this reading |

I was very pleased with your notes and question bank. I especially like the mock exams because it helped to pull everything together.

Martin Rockenfeldt

Learning Outcome Statements

explain how a bond's exposure to each of the factors driving the yield curve can be measured and how these exposures can be used to manage yield curve risks;

explain the maturity structure of yield volatilities and their effect on price volatility.

CFA® 2025 Level II Curriculum, Volume 4, Module 26.