Why should I choose AnalystNotes?

AnalystNotes specializes in helping candidates pass. Period.

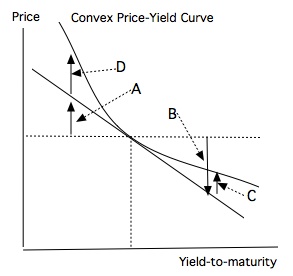

Basic Question 1 of 16

Refer to the following price-yield curve.

The estimated changes due to duration are represented by ______.

User Contributed Comments 2

| User | Comment |

|---|---|

| msusolar | can anybody explain? |

| CFAMay2022 | A&B reps changes in price due to change in YTM/slope of the tangent line (rather than actual changes on curve) |

I am happy to say that I passed! Your study notes certainly helped prepare me for what was the most difficult exam I had ever taken.

Andrea Schildbach

Learning Outcome Statements

calculate and interpret approximate convexity and compare approximate and effective convexity;

calculate the percentage price change of a bond for a specified change in yield, given the bond's approximate duration and convexity;

CFA® 2024 Level I Curriculum, Volume 5, Module 46.