- CFA Exams

- 2023 Level I > Topic 4. Corporate Issuers

- 4. Estimating Beta

Why should I choose AnalystNotes?

AnalystNotes specializes in helping candidates pass. Period.

Subject 4. Estimating Beta

The determination of cost of capital under the CAPM approach involves the estimation of β, risk-free rate, and market return.

Estimating Beta for Public Companies

The historical β is the first step in the determination of the ex-ante β.

The standard procedure for estimating βs is to regress stock returns (Ri)against market returns (Rmi = a + b Rm, where b is the slope of the regression and corresponds to the β of the stock. It measures the riskiness of the stock.

To estimate βi an analyst needs to make several choices:

- Which index should be used to represent the market portfolio? The S&P 500 is a traditional choice to represent U.S. equities.

- What should be the length of data period and the frequency of observations?

According to Blume, there is a tendency of betas to converge towards the mean of all betas.

It corrects the estimated β for its tendency to revert to 1. It adjusts β in such a way that it is closer to the expected β in the future.

Estimating Beta for Thinly Traded and Nonpublic Companies

If we are thinking of a new company for a single project, we will have no historical records to go by. We would then compute the β of companies of the same size and about the same lines of business and after making necessary adjustments, take this as the β for the firm. The pure-play method can be used to take a comparable publicly traded company's beta and adjust it for financial leverage differences.

The β that we impute to a project is likely to undergo changes with changes in the capital structure of the company. If the company is entirely equity-based, its β is likely to be lower than it would be if it undertakes borrowing.

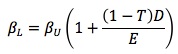

Let us call the β of a firm that is levered "levered β" and that of a firm on an all-equity structure "unlevered β."

β of a levered firm:

where:

βL = β of a levered firm

βU = β of an unlevered firm

T = tax rate

D = component of debt in capital structure

E = component of equity in capital structure

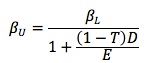

If the β of a firm is available and that β has been estimated on the premise that the firm is unlevered, we can now ascertain the β of the firm should it undertake some borrowing by using the following formula:

β of an unlevered firm:

In the same way, given the β of a firm which is already levered, we can ascertain what its β would be if it chooses an all-equity structure. This also means that if the target firm has leverage different from the structure assumed in estimating the levered β, this can first be converted into an unlevered β and then re-converted into a levered β using the leverage parameters relevant to the firm.

As a first step, we have to identify firms that reasonably resemble the project for which the beta is to be estimated. The stock β of these firms is then taken. Their respective leverage position (ratio of debt to equity) is also considered. After duly adjusting the tax factor and applying the above formula, we can determine the proxy β of the project assuming that it is unlevered.

The procedure is illustrated below:

Suppose there are three firms, P, Q, and R, which closely resemble project X (that is to be embarked upon). The stock betas of the three firms are taken and found to be 2.73, 2.23, and 1.73 respectively. The ratio of debt to equity for the three firms averages to 0.67. The marginal tax rate is 36%.

The average stock β works out to 2.23. Translating these numbers into the formula for unlevered firms, we get: βU = βL / (1 + (1 - T)(D/E)) = 2.23/(1+0.64 x 0.67) = 1.56.

This suggests that on an all-equity basis the β of the project would be 1.56. Now, if the project is proposed to be financed by 50% equity and 50% debt, we can modify the above β by applying the formula for levered firms:

βL = βU (1 + (1 - T) D/E) = 1.56 (1 + 0.64 x 0.5/0.5) = 2.56

So, on a 1:1 debt equity ratio, the β will be 2.56. This β can be used now for determining the cost of equity for the project and its weighted average cost of capital, to make a more meaningful appraisal.

Practice Question 1

If the estimated beta is 0.8, using Blume�s formula, the adjusted beta will be ______.

Correct Answer: 0.86

2/3 * 0.8 + 1/3 * 1 = 0.86

The Blume method is a method used to adjust the calculated beta. It is usually referred to as the forecasted beta.

This shows a slightly higher adjusted beta. This means that if the estimated(raw) beta is less than 1, then the adjusted beta will be greater than the estimated beta and also will be close to 1. And if the estimated(raw) beta is greater than 1, then the adjusted beta will be less than the estimated beta and also will be close to 1.

Practice Question 2

The decision to use a particular index to represent the market portfolio will affect the estimation of:I. equity risk premium.

II. beta estimate for a particular stock.Correct Answer: I and II

The decision affects both estimates.

The value of β estimated depends on a few choices too: which market index to be used? what's the data period? the frequency of observations?

Practice Question 3

Which statement(s) is (are) true regarding adjusted Beta?I. The mean-reverting level of the beta is 0.

II. If the historical beta is greater than 1, the adjusted beta will be more than the historical beta.Correct Answer: None of them

I. It is 1. II. It will be less than the historical beta.

Practice Question 4

Assume GE is evaluating an investment in the oil and gas industry. GE would examine existing firms that are pure plays (public firms operating only in the oil and gas industry). Let's say GE selects Berry Petroleum & Forest Oil as pure plays:

These firms are operationally similar, but Berry Petroleum's βE = 0.65 and Forest Oil's βE = 0.90. (Why are they so different? Forest Oil uses debt for 39% of financing; Berry Petroleum: 14%)

Assume:

- Risk-free rate of interest is 6%.

- Tax rate is 0%.

- The market's expected rate of return is 10%.

- GE's debt/equity ratio is 25%.

- Investors expect 6.5% on GE's bonds:

To determine the correct βA to use as discount rate for the project, GE must convert pure play βE to βA, then average.

Unlevered equity beta (which is the same as βA when taxes are zero) strips out the effect of financial leverage, so it is always less than or equal to equity beta.

Berry's βA = 0.56 and Forest's βA = 0.54, so average βA = 0.55.

GE's capital structure consists of 20% debt and 80% equity (D/E ratio = 0.25). Compute re-levered equity beta: βGE = βA (1 + D/E) = 0.55 (1 + 0.25) = 0.69.

The required rate of return on equity is 6% + 0.69 x (0.1 - 0.06) = 8.76%.

WACC = 20% x 6.5 + 80% x 8.76 = 8.308%

Practice Question 5

Which of the following statements is false?A. In the pure play method, a company finds several firms in the same line of business as the project being evaluated; it then averages those companies' betas to determine the cost of capital.

B. The pure play approach can only be used to evaluate major assets such as whole divisions.

C. The pure play approach can only be used to evaluate small assets.

D. The pure play approach is a technique used to measure the beta risk of investment projects.Correct Answer: C

The pure play method requires that the company find firms in the same line of business as the project being evaluated; this is virtually impossible for small assets.

Practice Question 6

Which statements are true?I. In the pure play method a firm averages the betas of companies that are in the same line of business as the project being evaluated.

II. The pure play method can only be used after a project has begun operation.

III. The pure play method estimates the beta of a project by using as a proxy the beta of a company that does nothing but the activity dictated by the project in question.Correct Answer: I and III

While a project's risk is incorporated into the risk of the company as a whole, its individual risk profile could be remarkably different from the risk profile of the company as a whole. The only time that a company's beta may be used as a proxy for a project's beta is when the project has a risk profile that is largely similar to that of the corporation as a whole.

Practice Question 7

The beta of Microsoft stock has been estimated as 1.5 by Merrill Lynch using regression analysis on a sample of historical returns. The Blume adjusted beta of Microsoft stock would be:A. 1.5

B. 1.0

C. 1.33Correct Answer: C

(2/3) * sample beta + 1/3 = 1.33.

Practice Question 8

Company PQR is in the telemarketing business. The asset beta for a comparable company in the same industry is 1.3. If company PQR's debt-to-equity ratio is 1.2, and the corporate tax rate is 35%, what is company QPR's equity beta?A. 1.65

B. 2.31

C. 2.58Correct Answer: B

Beta for a company that is not publicly traded may be estimated using the pure-play method. In the pure-play method, the starting point is the beta for a comparable publicly traded company, i.e., one which has similar business risk or risk relating to revenue uncertainty. This beta is then adjusted for differences in financial leverage to derive an estimate of beta for the company. Adjusting beta for financial leverage differences requires a process of "unlevering" and "levering" the beta.

The comparable company�s asset beta, BU,comparable, is given as 1.3. You are also provided with information which indicates that tcomparable = 35% and D/E = 1.2. Solving for BL,company = 1.3 � [1 + ((1-0.35) � 1.2)] = 1.3 � (1 + 0.78) = 2.314.

Practice Question 9

The choice of the length of period and the frequency of observation will affect the estimation of:A. Equity risk premium only.

B. Beta estimate for a particular stock only.

C. Both equity risk premium and the beta estimate for a particular stock.Correct Answer: C

The decision affects both estimates.

Study notes from a previous year's CFA exam:

4. Estimating Beta