- CFA Exams

- 2026 Level I

- Topic 3. Corporate Issuers

- Learning Module 6. Capital Structure

- Subject 2. Factors Affecting Capital Structure

Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 2. Factors Affecting Capital Structure PDF Download

A company's stage in the life cycle, its cash flow characteristics, and its ability to support debt largely dictate its capital structure since capital not sourced through borrowing must come from equity (including retained earnings).

Some businesses, such as real estate and other capital-intensive businesses, employ a lot of leverage regardless of their development stage. Some mature, large businesses may use little debt because they don't own large amount of fixed assets. Companies in cyclical industries and capital light businesses tend to have little debt in their capital structures.

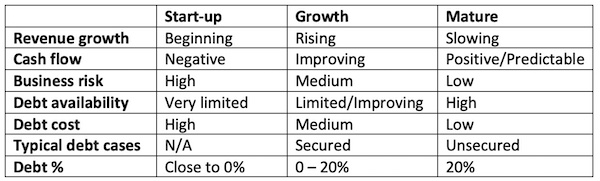

Corporate Life Cycle

Generally speaking, as companies mature and move from start-up, through growth, to mature, their business risk declines as operating cash flows turn positive with increasing predictability, allowing for greater use of leverage at more attractive terms.

Start-Ups: A company at this stage is a cash consumer, with negative revenues, negative cash flows and high business risks. Its main funding source is private equity, with almost no debt.

Growth Businesses: Revenue growth is high, and cash flows may turn positive and predictable. Asset-backed debt may be needed to finance its revenue growth, but equity remains the predominant source of capital.

Mature Businesses: Revenue growth slows down or even starts to decline. Cash flows are stable and predictable. Debt financing is preferred over higher-cost equity financing, partly due to the tax-deductibility of interest expense.

De-leveraging may occur, and share buybacks may be executed if the company has enough cash and the share price is right.

Determinants of the Costs of Debt and Equity

Investors consider both top-down factors, which impact the macroeconomic and industry levels, as well as factors that are specific to the particular issuer.

Top-down factors affect investors' expectations at a level beyond just one particular firm. Examples are risk-free rates, GDP growth, oil price. Some top-down factors can be positive or negative depending on the industry in which an issuer operates.

Issuer-Specific Factors include sales risks, operating leverage, financial leverage, and types of assets.

Leverage

Leverage is the extent to which fixed costs are used in a company's cost structure.

- Operating leverage is the extent to which fixed operating costs (e.g., depreciation, rent) are used in a firm's operations.

- Financial leverage is the extent to which fixed-income securities (debt and preferred stock) are used in a firm's capital structure.

Leverage affects a firm's risk, as it can magnify earnings both up and down. The bigger the leverage, the more volatile the firm's future earnings and cash flows, and the greater the discount rate applied in the firm's valuation (by bondholders and stockholders).

Operating Leverage

A company that has high operating leverage is a company with a large proportion of fixed input costs, whereas a company with largely variable input costs is said to have low operating leverage (due to its small amount of fixed costs).

A company with a high degree of operating leverage that has a small change in sales will experience a large change in profits and rate of return. This is due to the fact that because the company has a large fixed cost component, any increase in sales will cause an even greater increase in net income, since the fixed costs have already been incurred.

In many respects operating leverage is determined by technology. High (low) operating leverage is usually associated with capital (labor) intensive industries.

The degree of operating leverage (DOL) is defined as the percentage change in EBIT (operating income) that results from a given percentage change in sales. It measures the impact of a change in sales on EBIT.

Here Q is the number of units, P is the average sales price per unit of output, V is the variable cost per unit, F is fixed operating cost, S is sales in dollars, and VC is total variable costs.

For example, assume that a firm has sales of $100,000, variable costs of $50,000, and fixed costs of $20,000. Its DOL is (100,000 - 50,000) / (100,000 - 50,000 - 20,000) = 1.67.

Financial Leverage

Financial risk is the additional risk placed on the common stockholders as a result of the decision to use fixed-income securities (debt and preferred stock). Increases in financial leverage (the use of fixed-income securities) increases financial risk and the expected return of stockholders, due to the obligation of servicing the fixed interest payments.

The questions are: Is the increased rate of return sufficient to compensate shareholders for the increased risk? What is the optimal financial structure to maximize stock price and the firm's value?

Financial risk depends on two factors:

- Cash flow volatility. The more volatile (stable) a firm's cash flows, the higher (lower) the financial risk.

- Financial leverage. The higher the financial leverage, the higher the financial risk.

As a general proposition, financial leverage raises the expected rate of return, but at the cost of increased financial risk (and thus total risk). So, you are faced with a trade-off: if you use more financial leverage, you increase the expected rate of return, which is good, but you also increase risk, which is bad.

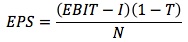

The degree of financial leverage (DFL) measures the financial risk.

It shows how a given percentage change in EBIT per share will affect EPS.

The equation above is developed as follows:

where:

I = interest paid

T = marginal tax rate

N = number of shares outstanding

I is a constant so ΔI = 0, therefore:

Now the percentage change in EPS is the change in EPS divided by the original EPS, which is:

DFL is defined as the percentage change in earnings per share (EPS) divided by the percentage change in EBIT.

Consider a company with EBIT = $100,000 and interest = $20,000. Its DFL = 100,000 / (100,000 - 20,000) = 1.25. Therefore, a 100% increase in EBIT would result in a 125% increase in EPS.

Unlike operating leverage, the degree of financial leverage is most often a choice by the company's management. Companies with a higher ratio of tangible assets to total assets may have higher degrees of financial leverage because lenders may feel more secure that their claims would be satisfied in the event of a downturn.

User Contributed Comments 17

| User | Comment |

|---|---|

| thud | How come EBIT = [Q(P - V)] in the business risk section and in the financial risk section it's [Q(P - V) - F]??? |

| xiong | Q (P - V) is the percentage change in EBIT. It has nothing to do with F. Q (P - V) - F is EBIT itself. |

| jd2442424 | The derivation of DFL stops short one step before the end. You also need to divide percent change in EBIT by the percent change in EPS ( delta EBIT / (EBIT - I) ) to get EBIT / (EBIT - 1). |

| chris76 | Q(P-V) is not the percentage change in Ebit...Nonetheless both formulas as presented are correct (a little algebra will confirm this) |

| johntan1979 | DOL: What is considered high and what is low? Is 1.67 (example in the notes) high? |

| johntan1979 | Towards the end of the notes, it is stated that "DFL is the %change in EPS divided by the %change in EBIT." I thought DFL = %change in NI / %change in EBIT? NI is definitely NOT = EPS, and I don't think they are interchangeable. |

| johntan1979 | Hmmm... just read from Kaplan's Schweser notes that the two are OK to be used interchangeably for DFL. So confusing! :( |

| gill15 | I just read the CFA curriculum book...just easier sometimes |

| robertucla | You have to compare dol to comparable firms in industry |

| RamaG | @jonathan : EPS = NI / # of share outstanding , since share float is constant , % change in EPS = % change in NI, so are interchangeable when considering % change |

| Shaan23 | This operating profit thing is confusing. If you do Q.5 in the last section or one of those Q's. We found operating profit for a question and used Q(P - V) but in this section it uses FC as well |

| jodyleesc | Can someone explain why %change in EBIT / %change in Sales = Q(P - V) / Q(P-V) - F ? |

| khalifa92 | those are two different equations to find DOL johntan higher DOL is caused bu graeter use of fixed operating cost relative to vc leads to more sensitivite in EBIT unit solds thus more risk |

| khalifa92 | you guys wake up Q(P-VC) or Q(P-VC) - F are mentioned in two different formulas with two different understanding the first one is the relation between operating profit to changes in unit sold the second one includes the first formula and moves down in the income statemet to take measure of the financial cost which leads to EBIT and relate it to net income and thus net income which in the end becomes all money the company can do whatever it wants with can become used to calculate EPS if they want to distribute it or keep it as retained earning thus they are interchangeable. |

| khalifa92 | but iam more confused because the second part of this LOS isnt in the book so ill ignore it for now. |

| unknown | Jodyleesc: Think about it as elasticity. %change Y / %changeX. By definition, EBIT = Q(P-V)-F and Sales = Q*P; When we do point elasticity, where dx->0, we have %changeY / %changeX = dY/dX * X/Y; if you take derivatives of EBIT and Sales with respect to Quantity, then dY= (P-V) and dX = P; thus (P-V)/P * X/Y = (P-V)/P*(Q*P/EBIT) = (P-V)*Q/EBIT = (P-V)*Q/ ((P-V)*Q-F) |

| MathLoser | @Jodyleesc: First: Calculate DOL using [Q(P-V)] / [Q(P-V)-F] Example: you have DOL = 3,0. Assume that your company has a 3% increase in sales. %change in EBIT = DOL x %change in sales = 3 x 3% = 9% That's the point of the formula. |

You have a wonderful website and definitely should take some credit for your members' outstanding grades.

Colin Sampaleanu

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add