- CFA Exams

- 2026 Level II

- Topic 2. Economics

- Learning Module 8. Currency Exchange Rates: Understanding Equilibrium Value

- Subject 2. Foreign Exchange Forward Markets

Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 2. Foreign Exchange Forward Markets PDF Download

In the spot market, currencies are traded for immediate delivery (which is actually two business days after the transaction has been conducted). In the forward market, contracts are made to buy or sell currencies for future delivery.

In a typical forward transaction, a U.S. company buys textiles from England with payment of £1 million due in 90 days. The importer is thus short GBP - that is, it owes GBP for future delivery. Suppose the present price of the GBP is $1.71. Over the next 90 days, however, the GBP might rise against the U.S. dollar, raising the U.S. dollar cost of the textiles. The importer can guard against this exchange risk by immediately negotiating a 90-day forward contract with a bank at a price, say, £:$ = 1.72. In 90 days the bank will give the importer £1 million and the importer will give the bank 1.72 million U.S. dollars. By going long in the forward market the importer is able to convert a short underlying position in GBP to a zero net exposed position.

Three points are worth noting:

- The gain or loss on the forward contract is unrelated to the current spot rate of £:$ = 1.71.

- The forward contract gain or loss exactly offsets the change in the U.S. dollar cost of the textile order that is associated with movements in the GBP's value.

- The forward contract is not an option contract. Both parties must perform the agreed-on behavior.

Forward exchange rates are often quoted as a premium, or discount, to the spot exchange rate. A foreign currency is at a forward discount if the forward rate is below the spot rate, whereas a forward premium exists if the forward rate is above the spot rate. Clearly, a negative premium is a discount.

For example, if the one-month forward exchange rate is $:€ = 0.80200 and the spot rate is $:€ = 0.80000, the $ quotes with a premium of 0.0020 €/$. In the language of currency traders, the $ is "strong" relative to the €.

Consequently, when a trader announces that a currency quotes at a premium (discount), the premium (discount) should be added to (subtracted from) the spot exchange rate to obtain the value of the forward exchange rate.

Forward points are often used in FX markets to quote forward exchange rates. To determine the forward rate, the number of basis points are subtracted from or added to the current spot rate. For example, if the current spot rate of USD/EUR is 1.2745, and the number of forward points is 50 for one-month USD/EUR forward, the forward rate is then 1.2745 + 0.0050 = 1.2795. In this case there is a forward premium.

Covered Interest Rate Parity

According the covered interest rate parity (IRP) theory, the currency of the country with a lower interest rate should be at a forward premium in terms of the currency of the country with the higher rate. In an efficient market with no transaction costs, the interest differential should be (approximately) equal to the forward differential.

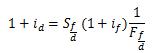

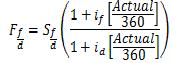

The exact relationship between the forward rate and the spot rate between two currencies is as follows:

- id is the domestic risk-free rate, and if is the foreign risk-free rate. They are both periodic interest rates, which should be computed as i = annual interest rate x number of days till the forward contract expires / 360.

- S is the spot rate, and F is the forward rate.

- It is assumed that there are no transaction costs.

Example

Suppose that the annual interest rate in the U.S. (foreign country) is 5%. The spot exchange rate $/£ = 1.50, and the 180-day forward rate is $/£ = 1.45. The U.S. periodic interest rate (180) is: 0.05 x 180 / 360 = 0.025. If interest rate parity holds:

1 + iUK = 1.5 (1 + 0.025)/1.45 => iUK = 6%.

Therefore, the annual UK interest rate is approximately 12%.

Similarly, you can calculate forward rate based on the two interest rates and spot rate.

Covered interest rate parity ensures that the return on a hedged (or "covered") foreign investment will just equal the domestic interest rate in investments of identical risk, thereby eliminating the possibility of having a money machine. When this condition holds, the covered interest differential - the difference between the domestic interest rate and the hedged foreign rate - is zero.

If the difference is not zero, covered interest rate arbitrage will generate profits without any risk or investment.

For example, suppose the interest rate on £ is 12% in London, and the interest rate on a comparable U.S.$ investment in New York is 7%. The £ spot rate is $/£ = 1.75 and the one-year forward rate is $/£ = 1.68. These rates imply a forward discount on £ of 4% [(1.68 - 1.75)/1.75] and a covered yield on £ approximately equal to 8% (12% - 4%). Suppose the borrowing and lending rates are identical and the bid-ask spread in the spot and forward markets is zero. An arbitrageur will:

- Borrow $1,000,000 in New York at 7%;

- Convert the $1,000,000 to £571,428.57 at £1 = $1.75;

- Invest the £571,428.57 in London at 12% for one year, and sell £640,000 forward at a rate of £1 = $1.68 for delivery in one year.

- At the end of the year, collect £640,000 from his investment in London, deliver it to the bank's foreign exchange department in return for $1,075,200, and use $1,070,000 to repay the loan in New York. The arbitrageur will earn $5,200 on this set of transactions with no investment at all.

FX Swap

An FX swap combines a spot and forward deal, with the two counterparts exchanging currencies today at the spot price but simultaneously contracting to repurchase them in the future at the forward price. A common, mid-market spot rate is used in the spot leg of the transaction. The bid-offer spread exists in the forward leg of the transaction. The longer the term of the forward contract, the larger the bid-ask spread.

Mark-to-Market Forward Contract

As forward FX rates in the market change, given a contract's set forward FX rate, the contract's market value fluctuates. Prior to the delivery time, a forward FX contract position may be liquidated in the open market at the position's mark to market value.

Example

After one month's time, a company in Spain has to mark-to-market a 3-month USD/EUR forward. To understand the concept and simplify the analysis let's ignore the bid-ask spread.

- On the date of the deal, the spot rate was 1.2763.

- The 3-month forward rate for the deal is 1.2880.

- The spot rate USD/EUR is now 1.2770. The 2-month forward rate now is 1.2990.

- The current 2-month risk-free interest rate is 4.8% (annualized).

The company bought EUR 1,000,000 against USD in 3 month. Now the company wants to close out the forward position. What is the market value of the forward today?

The company is committed to buy EUR 1,000,000 when the forward matures at 1.2880 in 2 months and pay USD 1,288,000. To close out its position it would sell EUR 1,000,000 at the 2-month forward rate of 1.2990, and would receive USD 1,299,000.

The cash-inflow of 1,299,000 - 1,288,000 = USD 11,000 would need to be discounted: 11,000 / (1 + 0.048/6) = USD 10,912.7.

User Contributed Comments 1

| User | Comment |

|---|---|

| Levancho | Thought FX Swap was no longer covered in this LOC |

Thanks again for your wonderful site ... it definitely made the difference.

Craig Baugh

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add