- CFA Exams

- CFA Level I Exam

- Topic 6. Fixed Income

- Learning Module 26. The Term Structure and Interest Rate Dynamics

- Subject 5. Yield Curve Factor Models

CFA Practice Question

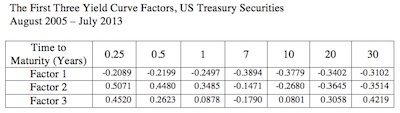

Which factor is most likely the change in the yield curve level?

A. Factor 1

B. Factor 2

C. Factor 3

Correct Answer: A

It shows for a one standard deviation positive change in that factor, the yield for a 0.25-year bond would decline by 0.2089%, a 0.50-year bond by 0.2199%, and so on across maturities, so that a 30-year bond would decline by 0.3102%. It describes approximately parallel shifts up and down the entire length of the yield curve.

User Contributed Comments 2

| User | Comment |

|---|---|

| ashish100 | Wtf wish they'd explain this better. AN please explain 100 dollars don't grow on trees brah |

| davidt87 | ashish100 i'm hating this section too. i guessed it because i assume a change in level of the curve will impact each rate in the same direction, and all of Factor 1 values were negative. Factor 2 appears to be steepness as you can see the shorter term rates are positive while the longer terms are negative - if you imagine how that would change a graph I think it would flatten it Factor 3 appears to be curvature because the middle is sinking and the short/long term values are positive Disclaimer: i have no fcking clue whats going on in this reading |