- CFA Exams

- CFA Level I Exam

- Topic 6. Fixed Income

- Learning Module 12. Yield-Based Bond Convexity and Portfolio Properties

- Subject 1. Bond Convexity and Convexity Adjustment

CFA Practice Question

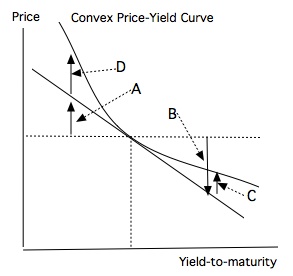

Refer to the following price-yield curve.

The estimated changes due to duration are represented by ______.

Correct Answer: A and B

C and D are estimated changes due to convexity.

User Contributed Comments 2

| User | Comment |

|---|---|

| msusolar | can anybody explain? |

| CFAMay2022 | A&B reps changes in price due to change in YTM/slope of the tangent line (rather than actual changes on curve) |