- CFA Exams

- CFA Level I Exam

- Topic 9. Portfolio Management

- Learning Module 38. Analysis of Active Portfolio Management

- Subject 2. Comparing Risk and Return

CFA Practice Question

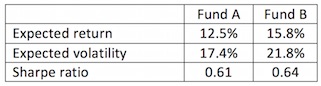

The risk-free rate is 1.8%. You have a choice of investing in two funds:

B. hold some cash and invest the rest in Fund B.

C. invest in both Fund A and Fund B.

You want to accept a maximum volatility of 17.4% only. You best option is to ______

A. invest in Fund A only.

B. hold some cash and invest the rest in Fund B.

C. invest in both Fund A and Fund B.

Correct Answer: B

The Sharpe ratio of Fund B is higher, so you want to invest in Fund B only. This is known as two-fund separation: an investor'??s portfolio should consist of two funds,?? one of which is the risk-free asset, and the other the risky asset portfolio with the highest Sharpe ratio.

User Contributed Comments 0

You need to log in first to add your comment.