- CFA Exams

- CFA Level I Exam

- Topic 9. Portfolio Management

- Learning Module 38. Analysis of Active Portfolio Management

- Subject 4. Applications of the Fundamental Law

CFA Practice Question

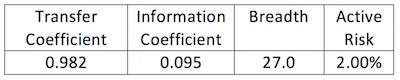

Here is the information about the Long-Short Global Equity Fund:

B. halved

C. the same

If the active risk were doubled to 4%, the information ratio would be ______.

A. doubled

B. halved

C. the same

Correct Answer: C

The expected active return would double, making the information ratio remain the same.

User Contributed Comments 0

You need to log in first to add your comment.