- CFA Exams

- CFA Level I Exam

- Topic 9. Portfolio Management

- Learning Module 38. Analysis of Active Portfolio Management

- Subject 3. The Fundamental Law of Active Management

CFA Practice Question

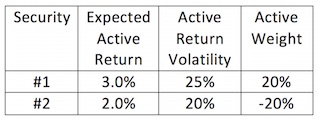

Consider two individual securities whose active returns are independent.

Suppose the benchmark portfolio for the two securities is equally weighted (50% for each security) and the forecasted return on the benchmark portfolio is 5%. According to the basic fundamental law, the information coefficient is ______.

Correct Answer: 0.3

#1: 50% + 20% = 70%, 5 + 3 = 8%

#2: 50% - 20% = 30%, 5 + 2 = 7%

The forecasted total return: 0.7 x 8% + 0.3 x 7% = 7.7%

The expected active return: 7.7% - 5% = 2.7%

Portfolio weights and total expected returns for each security:

#1: 50% + 20% = 70%, 5 + 3 = 8%

#2: 50% - 20% = 30%, 5 + 2 = 7%

For the managed portfolio:

The forecasted total return: 0.7 x 8% + 0.3 x 7% = 7.7%

The expected active return: 7.7% - 5% = 2.7%

The active risk of the managed portfolio: [0.22 x 252 + (-0.2) 2 x 202]1/2 = 6.4%

The information ratio (IR) = 2.7/6.4 = 0.42

According to the fundamental law, IR = IC (BR)1/2, 0.42 = IC x 21/2, IC = 0.3.

User Contributed Comments 1

| User | Comment |

|---|---|

| davidt87 | why wouldnt they keep 25 and 20 as percentage decimals? very confusing and unreliable way to work things out |