- CFA Exams

- CFA Level I Exam

- Topic 6. Fixed Income

- Learning Module 10. Interest Rate Risk and Return

- Subject 2. Macaulay Duration

CFA Practice Question

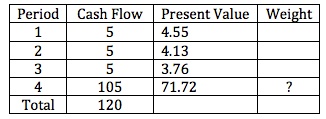

Consider a four-year, 5% annual coupon payment bond. Its yield to maturity is 10% and its price is 84.16 per 100 of par value.

B. 0.7172

C. 0.8522

To calculate Macaulay duration, what should be the weight of the last payment of 105?

A. 0.8750

B. 0.7172

C. 0.8522

Correct Answer: C

The total of present value is 84.16. The weight is 71.72/84.16 = 0.8522.

User Contributed Comments 1

| User | Comment |

|---|---|

| janglejuic | 71.72 / (4.55+4.13+3.76+71.72) |