- CFA Exams

- 2023 Level I > Topic 9. Portfolio Management > Reading 54. Technical Analysis

- 1. Major Return Measures

Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 1. Major Return Measures

There are various types of return measures.

-- beginning price: $100

-- dividends: $10

-- ending price: $150

-- beginning price: $300 (150 x 2)

-- dividends: $20 (10 x 2)

-- ending price: $280 (140 x 2)

- If the measurement period < 1 year, compound holding period returns to get an annualized rate of return for the year.

- If the measurement period > 1 year, take the geometric mean of the annual returns.

rannual = (1 + rperiod)c - 1

Holding Period Return

Refer to Reading 2 for a detailed discussion of this return measure.

Arithmetic or Mean Return

Refer to Reading 2 for a detailed discussion of this return measure.

Geometric Mean Return

Refer to Reading 2 for a detailed discussion of this return measure.

Money-Weighted Return or Internal Rate of Return

The dollar-weighted rate of return is essentially the internal rate of return (IRR) on a portfolio. This approach considers the timing and amount of cash flows. It is affected by the timing of cash flows. If funds are added to a portfolio when the portfolio is performing well (poorly), the dollar-weighted rate of return will be inflated (depressed).

The time-weighted rate of return measures the compound growth rate of $1 initial investment over the measurement period. Time-weighted means that returns are averaged over time. This approach is not affected by the timing of cash flows; therefore, it is the preferred method of performance measurement.

Example

Jayson bought a share of IBM stock for $100 on December 31, 2000. On December 31, 2001, he bought another share for $150. On December 31, 2002, he sold both shares for $140 each. The stock paid a dividend of $10 per share at the end of each year.

To calculate the dollar-weighted rate of return, you need to determine the timing and amount of cash flows for each year, and then set the present value of net cash flows to be 0: - 100 - 140/(1 + r) + 300/(1 + r)2 = 0. You can use the IRR function on a financial calculator to solve for r to get the dollar-weighted rate of return: r = 17%.

To calculate the time-weighted rate of return:

- Split the overall measurement period into equal sub-periods on the dates of cash flows.

For the first year:

-- beginning price: $100

-- dividends: $10

-- ending price: $150

- For the second year:

-- beginning price: $300 (150 x 2)

-- dividends: $20 (10 x 2)

-- ending price: $280 (140 x 2)

Calculate the holding period return (HPR) on the portfolio for each sub-period: HPR = (Dividends + Ending Price)/Beginning Price - 1. For the first year, HPR1: (150 + 10)/100 - 1 = 0.60. For the second year, HPR2: (280 + 20)/300 - 1 = 0.

Calculate the time-weighted rate of return:

- If the measurement period < 1 year, compound holding period returns to get an annualized rate of return for the year.

- If the measurement period > 1 year, take the geometric mean of the annual returns.

Annualized Return

Annualizing returns allows for comparison among different assets and over different time periods.

where c is the number of periods in a year and rperiod is the rate of return per period.

Example

Monthly return: 0.6%. The annualized return is (1 + 0.6%)12 - 1 = 7.44%.

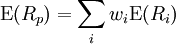

Portfolio Return

The expected return on a portfolio of assets is the market-weighted average of the expected returns on the individual assets in the portfolio.

where Rp is the return on the portfolio, Ri is the return on asset i and wi is the weighting of component asset i (that is, the share of asset i in the portfolio).

Other Major Return Measures

1. A gross return is the return before any fees, expense, taxes, etc. A net return is the return after deducting all fees and expenses from the gross return.

2. Different types of investments generate different types of income and have different tax implications. For example, in the U.S. the interest income is fully taxable at an investor's marginal tax rate while capital gains are taxed at a much lower rate. Therefore, many investors therefore use the after-tax return to evaluate mutual fund performance.

3. The nominal return and the real return are two ways to measure how well an investment is performing. The real return takes into consideration the effects of inflation when calculating how much buying power has changed.

4. An investor can also use leverage to amplify his expected return (and risk).

Practice Question 1

The semi-annual interest rate that equates the present value of the bond's cash flow to its current market price is 4.75%. It follows that ______I. the bond's horizon return is 9.35%.

II. the bond's effective annual yield is 9.73%.

III. the bond's yield-to-maturity is 9.50%.Correct Answer: II and III

Study notes from a previous year's CFA exam:

1. Major Return Measures