Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

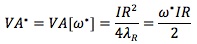

Subject 5. Value added: risk-adjusted residual return

The optimal portfolio P* lies at the point where the residual frontier is tangent to the preference line.

This implies that the ability of the manager to add value increases as:

- The square of the IR increases. In fact, the key to active management is the information ratio.

- The manager's risk aversion level decreases.

Given our risk aversion level, we all want the investment manager with the highest IR.

Practice Question 1

In seeking maximum value added, different investors will differ in:

A. IR: how high the information ratio to take.

B. λ: how aggressive of the investment strategy.

C. ω: how much residual risk to take.

They all seek the manager with the highest IR. A and B will determine the optimal level of residual risk to take.

Practice Question 2

The value added by a very good manager (IR = 0.75) with a conservative implementation (λ = 0.15) is:

A. 5%.

B. 1.25%.

C. 0.94%.

0.752/(4 x 0.15) = 0.9375%.

Practice Question 3

The key to active management is the:A. IR: information ratio.

B. λ: risk aversion level.

C. ω: residual risk level.Correct Answer: A

The value added is determined by IR and λ. The IR has a bigger impact on the value added.

Practice Question 4

The value added by a very good manager (IR = 0.75) with an aggressive implementation (λ = 0.05)is:A. 2.81%.

B. 15%.

C. 3.75%.Correct Answer: A

0.752/(4 x 0.05) = 2.8125%.

Study notes from a previous year's CFA exam:

5. Value added: risk-adjusted residual return