Why should I choose AnalystNotes?

Simply put: AnalystNotes offers the best value and the best product available to help you pass your exams.

Subject 5. The capital asset pricing model

- Investors only need to know expected returns, variances, and covariances in order to create optimal portfolios.

- Investors have homogeneous expectations: that is, they estimate identical probability distributions for future rates of return.

- All assets are marketable. The market for assets is perfectly competitive.

- Individual investors are price takers.

- Investors can borrow and lend any amount of money at the risk-free rate of return.

- There are no taxes or transaction costs involved in buying or selling assets.

The CAPM equation is:

where βi = Cov (Ri, RM) / Var (RM)

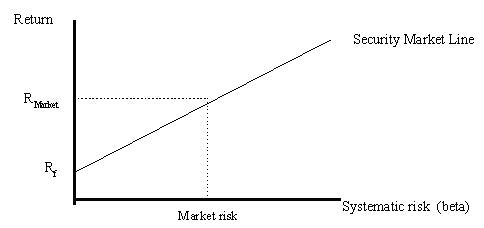

CAPM is used to determine the required rate of return for any risky asset. It uses the SML or security market line to compare the relationship between risk and return. Unlike the CML, which uses standard deviation as a risk measure on the X axis, the SML uses the market Beta, or the relationship between a security and the marketplace.

The use of beta enables an investor to compare the relationship between a single security and the market return, rather than a single security with each and every security (as Markowitz did). Consequently, the risk added to a market portfolio (or a fully diversified set of securities) should be reflected in the security's beta.

E(RM) - RF is the market risk premium, while the risk premium of the security is calculated by β(E(RM) - RF).

- The market portfolio has a β of 1.

- If β > 1, the security is more volatile than the market.

- If β < 1, the security is less volatile than the market.

The SML represents the required rate of return, given the systematic risk provided by the security. However, if the expected rate of return exceeds this amount, then the security provides an investment opportunity for the investor. The difference between the expected and required return is called the alpha (α) or excess rate of return. The alpha can be positive when the stock is undervalued (it lies above the SML), or negative when the stock is overvalued (it falls below the SML). The alpha becomes zero when the stock falls directly on the SML (properly valued).

Security Market Line vs. Capital Market Line:

- The CML examines the expected returns on efficient portfolios and their total risk (measured by standard deviation). The SML examines the expected returns on individual assets and their systematic risk (measured by beta). If the expected return-beta relationship is valid for any individual securities, it must also be valid for portfolios constructed with any of these securities. So, the SML is valid for both efficient portfolios and individual assets.

- The CML is the graph of the efficient frontier, and the SML is the graph of the CAPM.

- The slope of the CML is the market portfolio's Sharpe ratio, and the slope of the SML is the market risk premium.

- All properly priced securities and efficient portfolios lie on the SML. However, only efficient portfolios lie on the CML.

Practice Question 1

A risk free asset has:

I. a beta of zero.

II. a high yield.

III. a total risk of 1.

IV. no place in an efficient portfolio.

Practice Question 2

Capital asset pricing theory asserts that portfolio returns are best explained by:

A. economic factors.

B. diversification.

C. systematic risk.

Practice Question 3

Researchers were able to develop the CAPM by adding what variable to the efficient frontier?

A. Return on the market

B. Measure of risk

C. Risk-free rate

Practice Question 4

The SML relates:

A. expected return to standard deviation.

B. expected return of securities to expected return of portfolios.

C. efficient sets of portfolios to the risk-free rate.

D. expected return to beta.

E. standard deviation to risk.

Practice Question 5

Suppose the Technee Corporation's common stock has a beta of 1.2. If the risk-free rate is 5% and the expected market return is 8%, the expected return for Technee's common stock is:

A. 3.0%.

C. 6.0%.

C. 8.6%.

5 + 1.2(8 - 5) = 8.6%

Practice Question 6

Christopher owns two risky assets, both of which plot on the security market line. Asset A has an expected return of 12% and beta of 0.8. Asset B has an expected return of 18% and a beta of 1.4. If Christopher's portfolio beta is the same as the market portfolio, how much does he have invested in Asset A?

A. He has 1.33 invested.

B. He has 0.67 invested.

C. He has 1.67 invested.

Practice Question 7

The beta of a risk-free portfolio is:

A. 0

B. +1.0

C. -1.0

Practice Question 8

A stock with a beta of 1.5 should have a ______ required rate of return than the market, and a ______ required rate of return than a stock with a beta of 2.

A. higher, higher.

B. lower, lower.

C. higher, lower.

Practice Question 9

Which of the following statements about the security market line (SML) is (are) true?

I. The SML provides a benchmark for evaluating expected investment performance.

II. The SML leads all investors to invest in the same portfolio of risky assets.

III. The SML is a graphic representation of the relationship between expected return and beta.

IV. Properly valued assets plot exactly on the SML.

Practice Question 10

The Capital Asset Pricing Model (CAPM) is best described as:

A. the simple relationship between risk and return

B. the theoretical relationship between systematic risk and expected return

C. the graphical depiction of the risk/return relationship.

The CAPM is the theoretical relationship between systematic risk and expected return, which when graphed gives us the SML.

Practice Question 11

The Security Market Line (SML) is:

A. shows the risk-return relationship of the CAPM in well-functioning markets

B. is kinked when there is borrowing at rates higher than RF

C. a graphical depiction of the CAPM

The SML is the graphical representation of the CAPM, not the same thing as the CAPM. It is not dependent on the markets functioning well. The SML is not affected by different borrowing rates.

Practice Question 12

If a stock is over priced it would plot:

A. Above the security market line.

B. On the Y-axis.

C. Below the security market line.

Practice Question 13

The risk-free rate of return is 5%. The market portfolio (M) has an expected return of 16% and a standard deviation of 24%. The slope of the capital market line (CML) is:

A. 1

B. 0.46

C. 1.91

Slope = rise/run = (16% - 5%) / (24% - 0%) = 0.46

Practice Question 14

An individual security, Q, has covariance with the market portfolio, M, of 0.0750 (decimal). The expected return on the market portfolio is 15%, and its standard deviation is 24%. Security Q has a standard deviation of 40%. The beta for Q is:

A. 1.30

B. 0.77

C. 0.31

BetaQ = COVQ,M/VARM = 0.0750/0.242 = 1.30

Practice Question 15

Securities A and B have forecasted returns of 14% and 18% over the next 12 months. During the same period, the market (M) is expected to generate returns of 16%. If the risk-free rate is 6%, and βA = βB = 1.1, use the CAPM to determine whether the securities are correctly valued.

A. Both A and B are overvalued.

B. A is overvalued and B is undervalued.

C. B is overvalued and A is undervalued.

According to the CAPM, a security with a beta of 1.1 has a required return = 6% + 1.1(16% - 6%) or 17%. Therefore, A (expected return = 14%) is overvalued, and B (expected return = 18%) is undervalued.

Practice Question 16

According to the Capital Asset Pricing Model (CAPM), fairly priced securities

A. have positive betas.

B. have negative betas.

C. have zero alphas.

Practice Question 17

A portfolio consists of 45% of wealth invested in the market portfolio and the remaining in risk-free T-bills yielding 6.3%. The market portfolio has an expected return of 17% and a standard deviation of 19%. The beta of the portfolio is ______.A. 0.55

B. 0.45

C. 1.0Correct Answer: B

If your wealth is divided between the market portfolio and the risk-free asset, the portfolio beta equals the fraction invested in the market portfolio. It is instructive to prove this either by using the CAPM equation directly or by calculating the covariance between the portfolio and the market.

Practice Question 18

The capital asset pricing model (CAPM) states that:A. The expected risk premium on an investment is proportional to its beta

B. The expected rate of return on an investment is proportional to its beta

C. The expected rate of return on an investment depends on the risk-free rate and the market rate of return Correct Answer: A

Practice Question 19

Which of the following measurements can be found for a portfolio by simply taking the weighted average of the individual components?

I. Beta

II. Return

III. Standard deviation

A. I and II

B. II and III

C. I and IIICorrect Answer: A

Beta: a measurement of the volatility of a security with the market in general. A greater beta coefficient than 1 indicates systematic risk greater than the market, while a beta of less than 1 indicates systematic risk less than the market.

Practice Question 20

An upward sloping line in total risk-return space along which completely diversified portfolios plot, is calledA. security market line

B. efficient frontier

C. capital market lineCorrect Answer: C

Practice Question 21

Which of the following is (are) true about the Capital Market Theory?

I. A portfolio that lies above the Security Market Line (SML) is under-priced.

II. The correlation between two portfolios on the SML equals +1.

III. Portfolios that lie on the Capital Market Line (CML) are as completely diversified as possible.

IV. Portfolios that lie on the SML are not necessarily completely diversified.

A. I, III and IV

B. I, II, III and IV

C. I, II and IVCorrect Answer: A

The Capital Market line is a combination of the risk-free asset and the tangency portfolio that lies on the efficient frontier of risky assets. Hence, the CML consists entirely of efficient portfolios (and every single efficient portfolio must lie on the CML). Further, all the portfolios that lie on the CML are perfectly positively correlated. The SML, on the other hand, plots the expected return of a security against its beta. CAPM then implies that the SML is a straight line with the intercept representing the risk-free rate. Every single investment security that is fairly priced must lie on the SML. Thus, not every portfolio that lies on the SML is an efficient portfolio or completely diversified.

Practice Question 22

The slope of the SML in an economy is 8.9%. The risk-free rate prevailing in the economy is 4.9%. A security has a correlation coefficient of 0.23 with the market. The market's standard deviation is 15% while that of the security is 19%. The expected return on the portfolio equals ________.A. 14.19%

B. 7.49%

C. 13.66%Correct Answer: B

The Security Market Line (SML) is a plot of the expected returns on securities against their betas. CAPM implies that the slope of the SML equals the market risk premium and the intercept equals the risk-free rate. Hence, the data given in the problem imply that the market premium is 8.9%.

To calculate the expected return on the security using CAPM, we must first find its beta. The beta of the security equals the covariance between the security and the market divided by the market variance. Also, the covariance equals the product of the correlation coefficient and the individual standard deviations. Hence, the covariance between the security and the market equals 0.23 * 0.15 * 0.19 = 0.0066. Therefore, the beta of the security equals 0.0066/(0.152) = 0.29. Therefore, the CAPM expected return on the security equals 4.9% + 0.29 * 8.9% = 7.49%.

Practice Question 23

Assume that a security is fairly priced and has an expected rate of return of 0.13. The market expected rate of return is 0.13 and the risk-free rate is 0.04. The beta of the stock isA. 1.7

B. 1

C. 0Correct Answer: B

Since it is fairly priced and its expected rate of return is equal to that of the market portfolio, its beta must be 1.

Practice Question 24

You invest 50% 0f your money in security A with a beta of 1.6 and the rest of your money in security B with a beta of 0.7. The beta of the resulting portfolio isA. 1.4

B. 1.15

C. 1.08Correct Answer: B

0.5 x 1.6 + 0.5 x 0.7 = 1.15.

Practice Question 25

Without violating the rules of CAPM, which of the following strategies may be undertaken in an attempt to earn a return that's greater than that of the market?A. Short sell securities that have a beta of less than one and purchase the market portfolio.

B. Purchase securities that have a higher standard deviation than that of the market.

C. Purchase securities whose correlation coefficient with that of the market is greater than one.Correct Answer: A

Short selling is a form of borrowing . Therefore by borrowing to invest in the market portfolio, you increase the leverage in the portfolio and consequently, its beta. However, according to CAPM, this higher beta should lead to higher expected returns.

Practice Question 26

Stock A has a standard deviation of 16% and a beta of 1.1. T-bills are currently yielding 3.7% on an annualized basis. The expected return on the market index is 9.1% while its standard deviation is 14.9%. If Stock B is expected to earn 10.51% and it is of equal risk to Stock A, which of the following statements would be the most accurate?A. Since Stock A has an expected return of 11.41%, it must be overpriced.

B. Since Stock A has an expected return of 9.64%, it must be underpriced.

C. Since Stock A has an expected return of 9.64%, it must be overpriced.Correct Answer: C

Step 1. Calculate the expected return on Stock A: E(R) = (.10)(12%) + (.25)(15%) + (.40)(8%) + (.25)(-9%) = 5.9%

Step 2. Relative Comparison: Stock A's E(R) is 9.64%, and stock B's E(R) is 10.51%.

Step 3. Conclusion: Stock A is overpriced (this results a lower expected return.)

Study notes from a previous year's CFA exam:

5. The capital asset pricing model