- CFA Exams

- 2026 Level II

- Topic 6. Fixed Income

- Learning Module 26. The Term Structure and Interest Rate Dynamics

- Subject 3. The Swap Rate Curve and the Swap Spread

Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

Subject 3. The Swap Rate Curve and the Swap Spread PDF Download

A swap is an agreement to "swap" periodic fixed interest payments with floating interest payments. This kind of contract enables one to swap fixed liabilities into floating, and may be used to reflect your view of the market.

The swap market offers a variety of advantages. It has almost no government regulations, making it more comparable across different markets; some sovereign issues offer a variety of tax benefits to domestic and/or foreign investors, making government curve comparative analysis across countries latently inconsistent. In many countries there is simply no liquid government bond market with maturities longer than 1 year. The swap market is an increasingly liquid market, with narrow bid-ask spreads and a wide spectrum of maturities. The supply of swaps is solely dependent on the number of counterparties wishing to transact at any given time. No position in an underlying asset is required, avoiding any potential repo specials effects.

The swap rate is the interest rate for the fixed-rate leg of an interest rate swap. The swap curve is the swap's equivalent of a yield curve. It identifies the relationship between swap rates at varying maturities. Used in similar manner as a bond yield curve, the swap curve helps to identify different characteristics of the swap rate versus time.

Calculate Swap Rate

A par swap rate is the rate on the fixed leg of a "vanilla" interest rate swap for the relevant maturity. Spot rates, swap rates and discount factors can all be determined from each other.

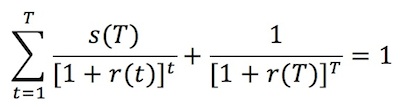

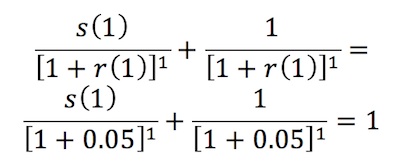

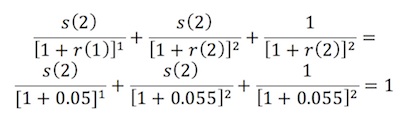

Let s(T) stand for the swap rate at time T.

Example

Let r(1) = 5%, r(2) = 5.5%, r(3) = 6% and r(4) = 6.5%.

For T = 1,

Therefore, s(1) = 5%.

For T = 2,

Therefore, s(2) = 5.49%.

For T = 3,

Therefore, s(3) = 5.97%.

Swap prices are frequently quoted as a spread over government issues, therefore serving as a rough indicator of credit and liquidity components of a bond's yield to maturity. A swap spread is the difference between the fixed rate on an interest rate swap contract and the yield on a on-the-run government bond with an equivalent tenor. It is usually, but not always, positive. Risk increases as the swap spread widens.

The swap spread is based on a bond's yield to maturity. The Z spread uses the zero-coupon yield curve instead. It is the constant basis point that would need to be added to the implied spot yield curve such that the discounted cash flows of a bond are equal to its current market price. It is a purely theoretical concept designed to allow a bond yield to be compared to a swap rate as fairly as possible.

The TED spread is the difference between the interest rates on interbank loans and on T-bills. It is an indicator of perceived credit risk in the general economy, since T-bills are considered risk-free while LIBOR reflects the credit risk of lending to commercial banks.

The LIBOR-OIS spread is the difference between LIBOR and OIS rates. It is considered to be a measure of risk and liquidity in the money market. A higher spread is typically interpreted as indication of a decreased willingness to lend by major banks.

User Contributed Comments 7

| User | Comment |

|---|---|

| gremlin | I've read that the asset-swap spread is really the coupon of an annuity in the swap market that equals the difference between the market price of the bond and the value of the bond when cash flows are valued using zero-coupon swap rates. Let's use a 5-Year Bond with 6% coupon having semi-annual payments whose current price is 99.41 making it have a YTM of 6.23%. Years Zero Swap Rates 0.5 4 1 4.1 1.5 4.2 2 4.3 2.5 4.35 3 4.4 3.5 4.45 4 4.5 4.5 4.55 5 4.6 To calculate I-spread you simply take the difference between YTM and 5yr Swap Rate and you arrive at 163bps To calculate Z-spread you use iteration or GoalSeek in Excel and you arrive at 166bps To calculate asset-swap spread I first calculate the value of the bond by discounting CFs by the zero swap rates and I arrive at 106.54. The difference between this value and the market value of the bond is 7.13 I use iteration or GoalSeek in Excel to find the coupon, that when discounted by the zero swap rates, would sum to 7.13 and I arrive at 80.1771bps at which point I multiply the result by 2 to make it annual. I therefore arrive at 160.35. From what I understand, this 160.35 figure would be the spread that would be added to Libor if the investor wanted to get into an asset swap to transform his 6% fixed rate bond into a floating rate bond. |

| mfecfa | the main difference between Z-spread and asset swap spread is Z-spread assumes constant credit spread through out the bond, while the asset swap is more "the market". I recently read some research by credit derivative IB that shows many more IG names are now inverted credit spread curves, based off CDS markets. For instance CFC may be trading at 1100bps for 2 year CDS, 900bps 5 yr , 850 bps 7 yr and 600bps 10yr. To "arb" this you would need to use the asset spread model on the cash bond, but then again, things can get worse before they get better, and you are really left with mark to market risk & counterparty risk, but I see certain bonds are paying 100bps+ for this. sounds like a good trade to me. |

| gremlin | I don't quite follow. so you're saying a quoted asset swap spread is an average spread across an entity's credit term structure? If that's what you're saying I respectfully disagree. If you wanted to "arb" the positive slope and negative slope between cash and CDS, traders would use the z-spread not the asset swap spread, but as you note the discrepancy can get bigger or persist even though the entry is attractive currently. |

| mfecfa | nope that is not what i said, not even close. more like the opposite. |

| connor | The LIBOR-OIS spread is considered a key measure of credit risk within the banking sector. LIBOR is the average interest rate that banks charge each other for short-term, unsecured loans. OIS, meanwhile, represents the assumed Fed Funds rate - the key interest rate controlled by the Federal Reserve - over the course of certain period. The LIBOR-OIS spread represents the difference between an interest rate with some credit risk built in and one that is virtually free of such hazards. Therefore, when the gap widens, it's a good sign that the financial sector is on edge. |

| epfrndz | Thanks for explaining the significance of the Libor-OIS spread, Connor. Makes more sense now |

| yuxdhk | Isn't LIBOR applying multiple currencies? Is your explanation only applying to USD LIBOR? LIBOR and OIS spread reflects the difference between the willingness and reality of the interbank borrowing. LIBOR is based on the rates that banks WOULD lend but OIS is based on the weighted average of the interbank transactions done during the date at the EOD. In this sense, LIBOR could be manipulated but OIS could not be. |

Your review questions and global ranking system were so helpful.

Lina

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add