- CFA Exams

- 2026 Level II

- Topic 1. Quantitative Methods

- Learning Module 5. Time-Series Analysis

- Subject 4. Unit Roots for Time-Series Analysis

Why should I choose AnalystNotes?

AnalystNotes specializes in helping candidates pass. Period.

Subject 4. Unit Roots for Time-Series Analysis PDF Download

An AR(1) series is said to be covariance stationary if the absolute value of the lag coefficient b1 is less than 1. If the absolute value of b1 = 1, the time series is said to have a unit root.

All random walks have unit roots since they have b1 = 1. This implies that they are not covariance stationary; hence we cannot apply the standard linear regression to test for b1 = 1.

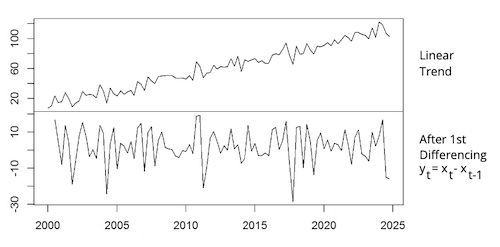

First Differencing

If we believe a time series is a random walk i.e. has a unit root, we can transform the data to a covariance stationary time series using a procedure called First Differencing. It involves subtracting the dependent variable in the immediately preceding period from the current value of the time series to define a new dependent variable, y.

Note that by taking first differences, you model the change in the value of the dependent variable. AR(1) yt = b0 + btyt-1 + εt

If b0 = b1 = 0, then yt = εt and εt = xt - xt-1, then yt = xt - xt-1 = εt

This transformed time series has a finite mean reverting level of b0/(1 - b1) = 0 and is therefore covariance stationary.

This is how first differencing removes the upward trend.

A properly differenced random walk time series is covariance stationary with a mean reversion level of 0.

The Unit Root Test for Nonstationary

If an AR (1) model has a coefficient of 1, it has a 'unit root' and no finite mean reverting level i.e. it is not covariance stationary. By definition, all Random Walks with or without a drift term have unit roots. Dickey and Fuller (DF) transform the AR (1) model to run a simple regression.

Rather than directly testing whether the original coefficient is different from 1, they test whether the new transformed coefficient (b1 - 1) is different from 0 using a modified t-test. In their actual test, Dickey and Fuller use the variable g = b1 - 1.

H0: g = 0. Time series has Unit Root (Not Stationary)

H1: g < 0. Time series doesn't have a Unit Root (Stationary).

If g is not significantly different from 0, then b1 = 0, the series must have a unit root. The null hypothesis will be rejected if the time series does not have a unit root. On the other hand, failure to reject the null hypothesis means that the time series has a unit root.

User Contributed Comments 0

You need to log in first to add your comment.

I am using your study notes and I know of at least 5 other friends of mine who used it and passed the exam last Dec. Keep up your great work!

Barnes

My Own Flashcard

No flashcard found. Add a private flashcard for the subject.

Add